As U.S. inflation has been waning through most of 2024, talk of possible interest rate cuts has risen in prominence in recent months. The FED, indeed, lowered the costs of borrowing by 50 basis points (BPS) following its September Federal Open Market Committee (FOMC) meeting.

Though hopes were high for a time that this year would see more substantial cuts, several reports in early October have significantly skewed expectations toward a reduction no greater than 25 BPS.

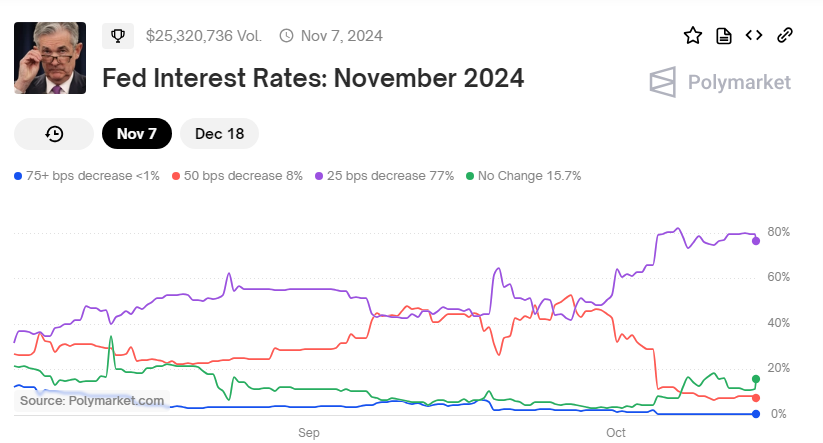

Finally, by October 14, 2024, the markets had again started pricing in the chance that the next FOMC meeting – scheduled for November – would bring no further cuts.

Specifically, a Polymarket betting event on the upcoming meeting shows a 16% chance of the funds rate remaining the same after the upcoming meeting.

Simultaneously, the prediction market estimates the odds of a modest 25 BPS reduction at 77%, and the odds of a 50 BPS cut have fallen to just 8%.

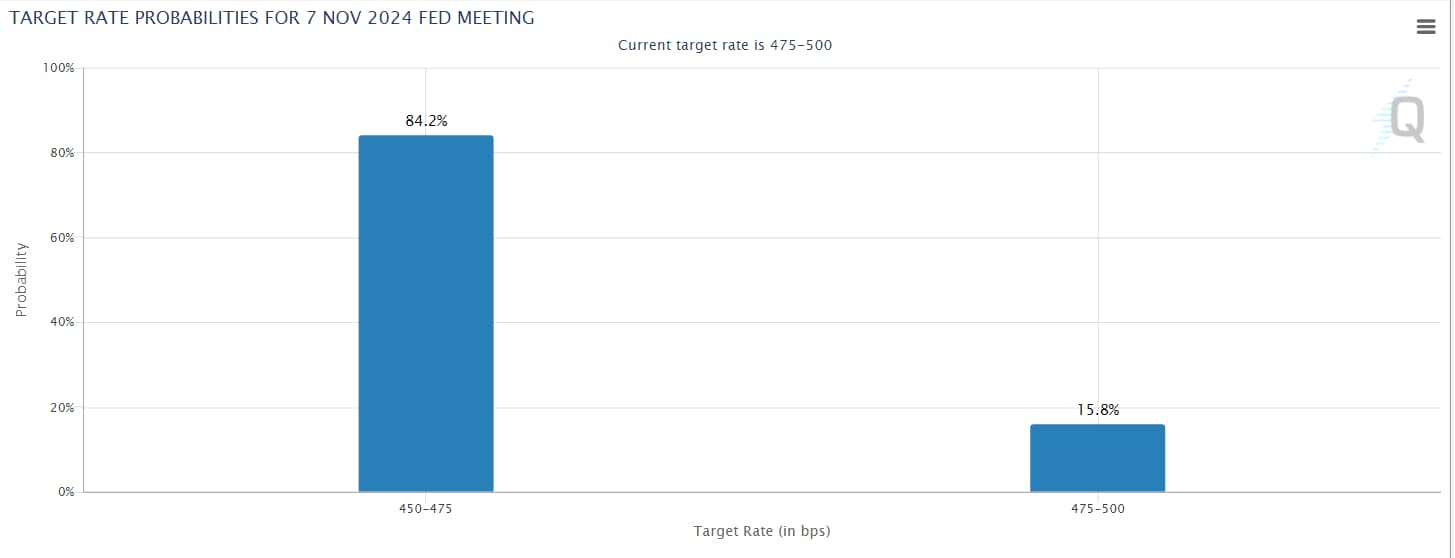

CME Fedwatch shows no chance of 50 BPS cut

The expectations seen in the prediction market are also backed by data retrieved from CME Group’s Fedwatch tool.

Indeed, Fedwatch shows that, at press time, there is a 15.8% chance of the interest rate remaining the same after the upcoming meeting and estimates the odds of a 25 BPS reduction at 84.2%.

Unlike on Polymarket, the implied odds for a cut of 50 BPS or greater are 0% on CME’s tool, a stark change from several weeks ago.

Why FED is increasingly likely to keep interest rates level

The new alignment of rate cut odds follows a sequence of reports that demonstrate the economy is no longer in dire need of stimulation. Simultaneously, they showed the danger of reigniting inflation remains present.

Indeed, the latest employment report vastly exceeded expectations, revealing that the U.S. created 254,000 jobs – significantly above the forecasted 150,000.

Simultaneously, the CPI print came in hotter than expected at 2.4%, slightly above the predicted 2.3%.

Finally, some experts, including Ed Yardeni – president of Yardeni Research – have also pointed toward the rapid increase in bond yields from 3.6% to 4% in the wake of the September cuts as a likely indication that America’s central bank will not reduce the funds rate further before the end of 2024.

Why FED cut rates in September

The Federal Reserve’s September decision to institute the first interest rate cut since 2020 followed two consecutive disappointing jobs reports, a dire manufacturing report, several major stock market pullbacks, and a more general fear that the U.S. economy has begun buckling under the high borrowing costs.

Still, as the more recent figures have shown, and as FED’s own Bostic opined, the central bank will likely keep the rates level through the rest of 2024.

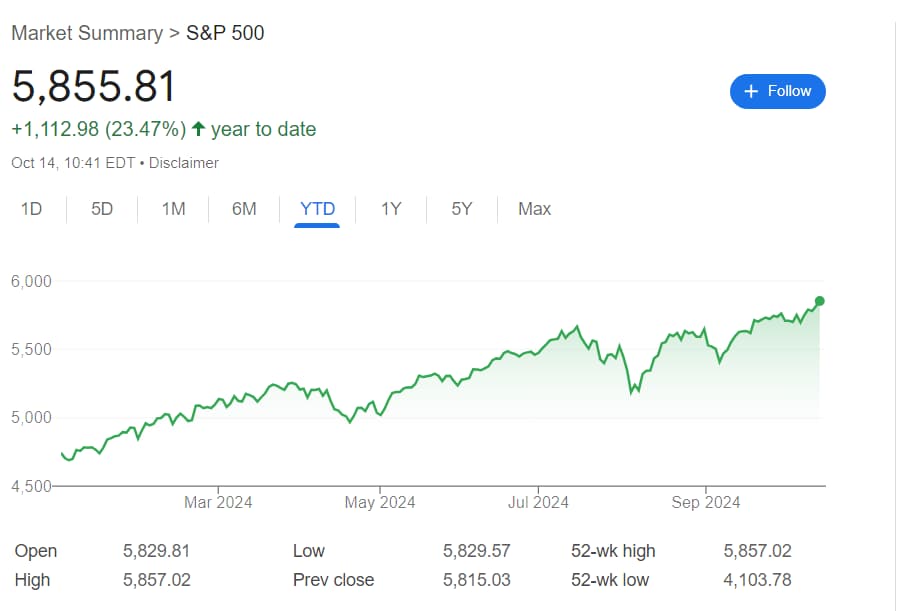

Such a notion is further bolstered by the fact that even before the September decision, U.S. stocks – as best exemplified by the benchmark S&P 500 index, which is 23.47% in the green year-to-date (YTD) – had been surging in 2024, thus largely invalidating the fears that continued tight conditions would trigger a recession.

Finally, it is worth pointing out that not all have welcomed the 50 BPS reduction. Multiple analysts – including Gordon Johnson of GJL Research, otherwise best known as a major Tesla (NASDAQ: TSLA) bear – have warned that conditions are not tight enough and that the FED’s metrics do not reflect the conditions faced by ordinary Americans.